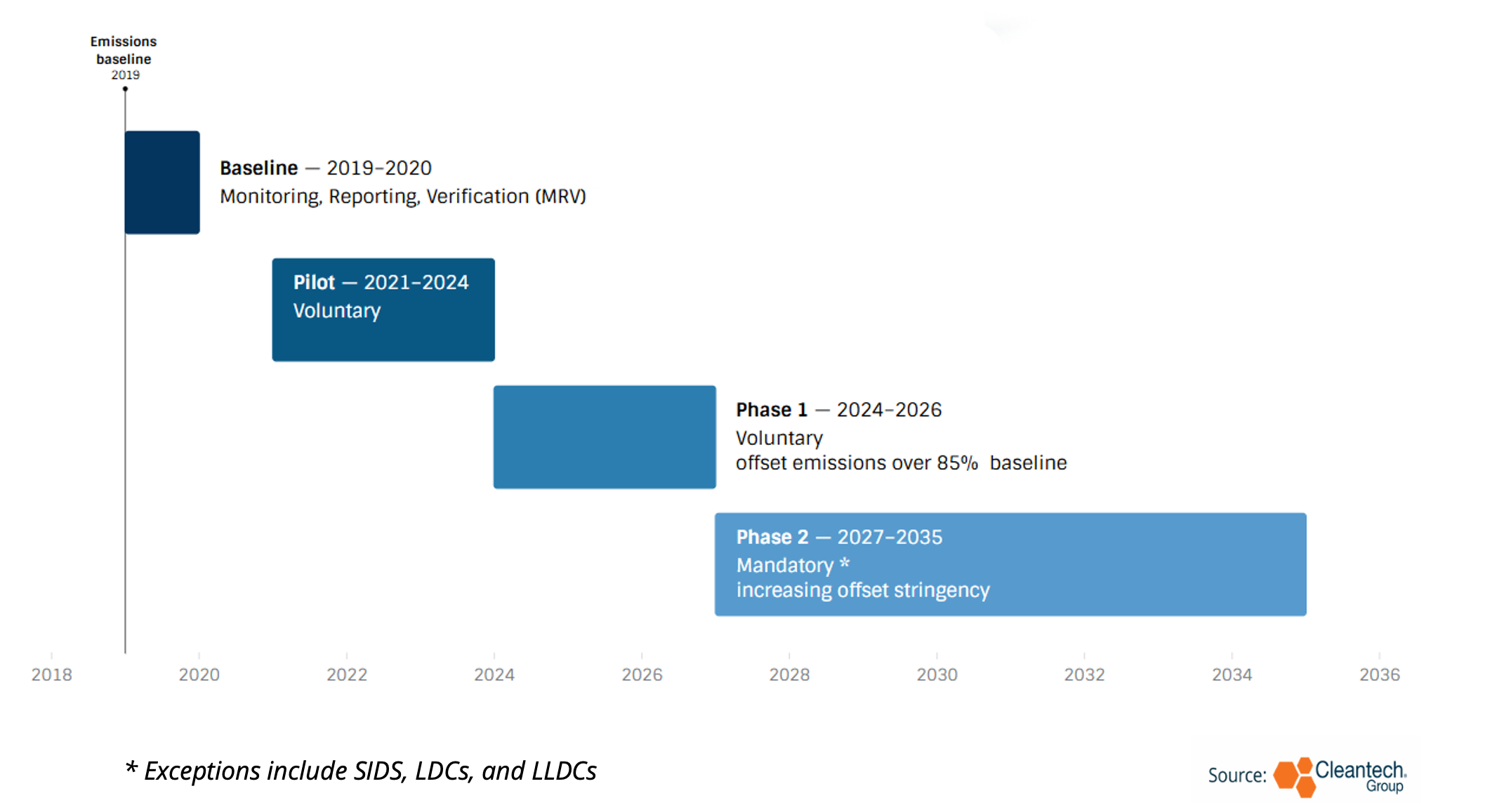

The aviation sector finds itself getting ready to a sustainability transition. This isn’t a shock. The Worldwide Civil Aviation Group (ICAO´s) carbon offsetting scheme CORSIA got here into impact in 2019, requiring airways to observe and report emissions. The primary (voluntary) offsetting section begins this 12 months and can run till 2026 and in 2027 offsetting mandates come into play for many worldwide flights.

CORSIA Phases and Timeline

As airways and carriers confront the incoming emissions offsetting mandates, complementary decarbonization insurance policies are coming into play as properly, particularly ReFuel EU, the EU´s sustainable aviation gas (SAF) minimal uptake necessities. Starting in 2025, flights leaving Europe should make the most of gas with a minimal of two% SAF, growing to six% by 2030, 20% by 2035, and 70% by 2050. SAF will undoubtedly be a crucial piece to the aviation decarbonization puzzle — projections counsel that it might displace greater than 65% of industry-wide emissions.

Whereas regulation implementing these targets is a promising step, the looming 2% uptake mandate is looming nearer, and SAF manufacturing and uptake is dealing with important feedstock and manufacturing bottlenecks. As innovators work to deal with these challenges, airways, fleet operators, and carriers are evaluating low- and zero-emissions plane options that complement SAF uptake, scale back gas consumption and emissions, and supply further financial alternatives.

Decarbonization Options: Aircrafts

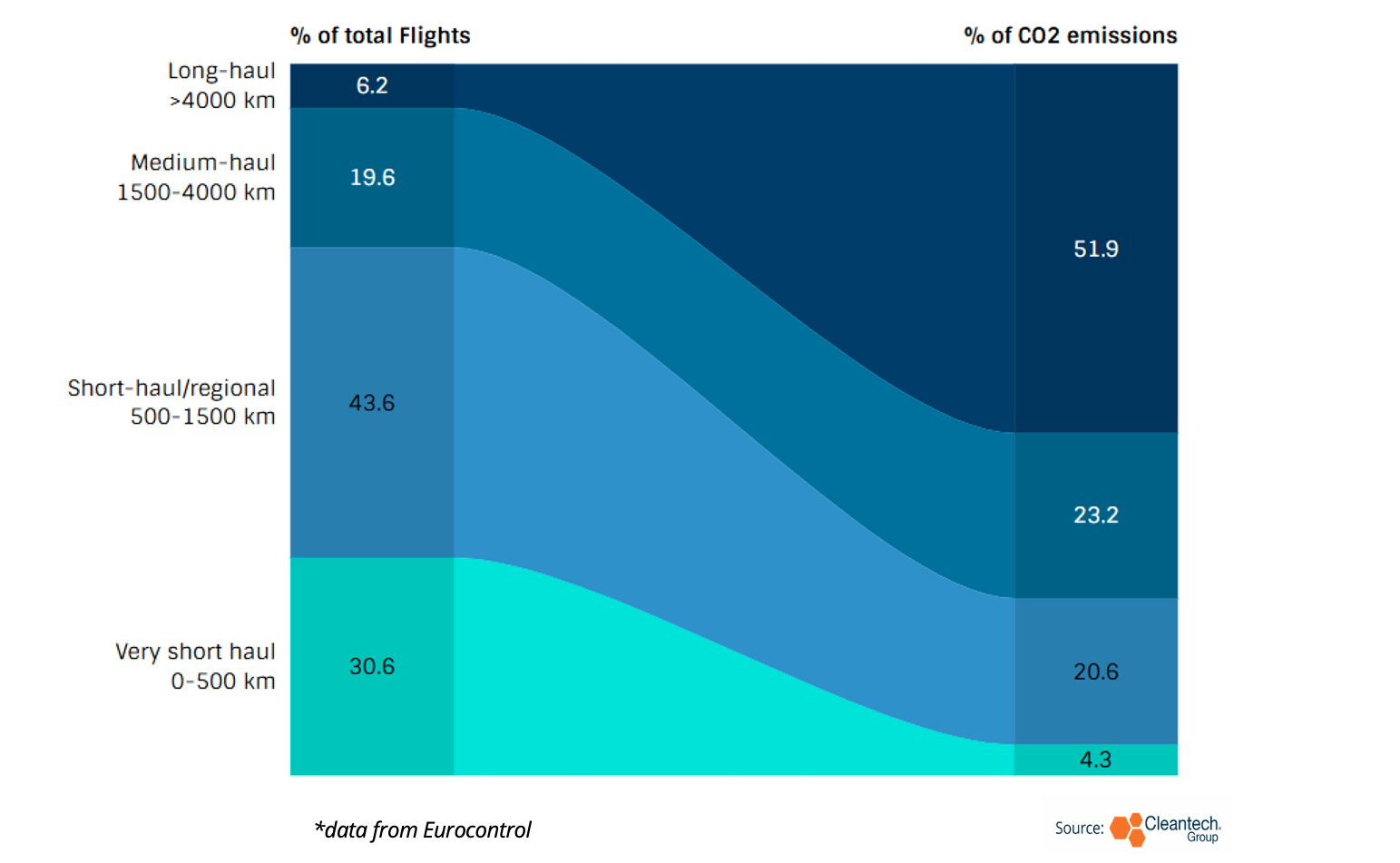

SAF will almost definitely be the one sensible resolution to decarbonize the biggest aircrafts and longest flights. Nevertheless, whereas provide stays low and the cost-premium of SAF exorbitantly excessive, electrical, hybrid, and hydrogen aircrafts present extra cost-efficient options for smaller aircrafts and shorter flights, prioritizing SAF use for essentially the most tough to abate routes (e.g., very long-haul flights). These options scale back prices and supply further financial alternatives for carriers.

Emissions Contribution of Flights by Size

Key Classes of Zero- or Low-emissions Aircrafts

Battery-electric aircrafts

- Professionals: Highest vitality effectivity of all options, confirmed and mature know-how and parts, decrease operations prices

- Cons: Vary and plane measurement severely restricted by battery weight

- Key innovation and path ahead: Scaling of aircrafts to 50-150 seat aircrafts and improve in vary from roughly 800 km to over 1000 km

Totally electrical aircrafts shall be restricted to very small (roughly 9–19-seater) commuter aircrafts, eVTOLs, and unmanned aircrafts even with important developments in battery vitality density. Hybrid aircrafts, nevertheless, are far more versatile, can scale to a lot bigger aircrafts, and add important emissions discount (40%+).

Critically, innovators are creating hybrid aircrafts which might be appropriate each with SAF and a spread of battery, electrical, and hydrogen propulsion applied sciences. This flexibility will allow carriers to combine whichever decarbonization options are most cost-efficient. When mixed with SAF, aircrafts can attain full emissions reductions whereas considerably decreasing SAF prices by decreasing gas consumption (e.g., Coronary heart Aerospace´s hybrid plane offers 40-100% gas discount relying on flight size).

Hydrogen aircrafts

- Professionals: Potential for for much longer vary and bigger plane measurement than battery-electric, improved vitality effectivity of hydrogen use in comparison with SAF

- Cons: Decrease know-how and element readiness than battery electrical plane’s lengthy and complicated certification course of, hydrogen infrastructure buildout required

- Key innovation and path ahead: Commercialization of hydrogen propulsion system and parts, development in storage and hydrogen gas cells

Hydrogen aircrafts are a divisive matter. On one hand, they may resolve a number of of the important thing challenges dealing with battery-electric aircrafts, particularly the difficulty of vitality density. Alternatively, challenges reminiscent of hydrogen storage, security, infrastructure buildout, and the general availability and price of inexperienced hydrogen elevate query marks and are sources of uncertainty.

Innovators reminiscent of ZeroAvia are creating superior gas cells, hydrogen propulsion programs, and bringing hydrogen aircrafts and parts to market extra shortly by hybrid plane retrofits. Though hydrogen aircrafts won’t be market prepared as quickly as electrical and hybrid-electric choices, incumbents and company buyers are investing considerably and fascinating with innovators and element builders attributable to hydrogen aircrafts´ long-term potential to decarbonize regional, short- and medium-haul routes.

Plane design and airships

- Professionals: Speedy excessive emissions discount (50-80%), unlocks airfreight financial alternatives, confirmed and market-ready know-how and parts, can use current infrastructure

- Cons: New-builds costlier than retrofits, slower overturn in plane fleets slows market uptake

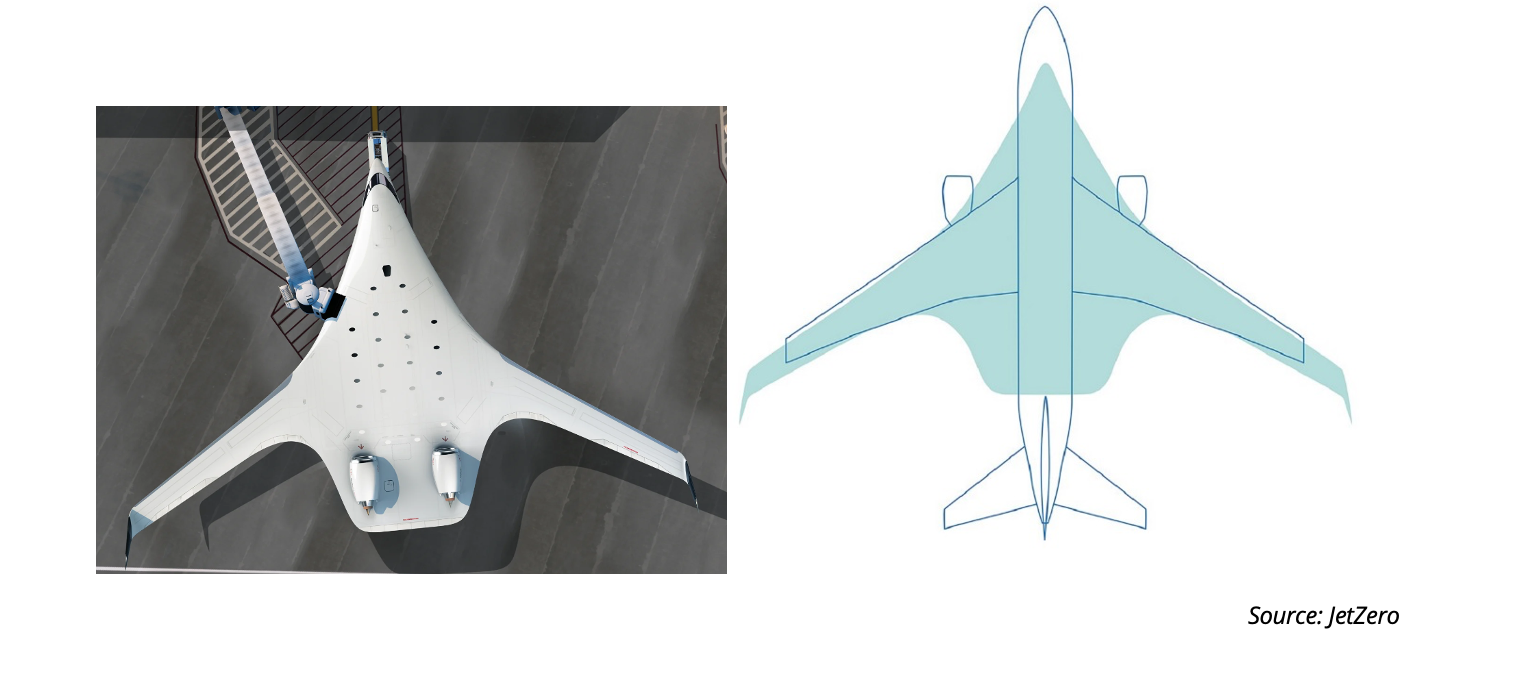

Standard aircrafts make the most of a tube-and-wing design we’re all acquainted with. Nevertheless, novel plane designs reminiscent of blended wing-body enhance aerodynamics and scale back drag, growing vary and payload. Innovators estimate between 50% and 80% discount in gas consumption and emissions (e.g., JetZero, Natilus) with the potential to achieve full emissions discount when mixed with electrical propulsion, inexperienced hydrogen, or SAF.

Idea of Blended Wing-body Plane and Comparability to Standard Plane

Airships are one other “novel” plane design. Although not a brand new idea, innovators are creating airships that leverage helium to generate elevate, decreasing gas and vitality consumption by 75% (100% when paired with zero-emissions propulsion or SAF. Whereas airship builders reminiscent of Hybrid Air Automobiles are approaching each the passenger and cargo markets, they’ve recognized airfreight as a key area of interest marketplace for early adoption.

Airships require minimal runway and infrastructure in comparison with typical airplanes, unlocking freight operations for small, distant, and tough to entry airports. Moreover, they aim the 20% of aviation emissions attributable to airfreight.

Key Takeaways:

- SAF alone won’t be ample to decarbonize aviation: electrical, hydrogen, and novel plane designs present cost-effective options for shorter flights and smaller aircrafts

- Uptake of those applied sciences and SAF will allow prioritization of SAF use for long-haul flights whereas decarbonizing remaining 95% of flights (shorter haul, smaller aircrafts)

- As battery, zero-emissions propulsion, and hydrogen element know-how improves, options may be scaled as much as longer flights and bigger aircrafts

- Hybrid options shall be quickest to market attributable to shorter certification processes and integration into fleet improve schedules

- Options which might be technologically confirmed and supply clear operations price reductions and futureproofing (e.g., compatibility with electrical, hydrogen, and SAF) are most engaging to airways

- Expertise and certification hurdles stay for hydrogen aircrafts, however funding and engagement from incumbents stays sturdy attributable to long-term potential

For an in-depth look on SAF and eJet innovation, see previous publications: Innovation Takes Flight with SAF and SAF: the Rise of eJet.