December greetings from Fraser, Colorado (picured), Cedar Rapids, Iowa, and Kansas Metropolis, Missouri. We hope the Holidays have been restful and satisfying for every of you, and that 2025 brings skilled and private progress.

For the primary time in a very long time (11 consecutive years excluding COVID-2021), Jim won’t be attending the Shopper Electronics Present (CES) in Las Vegas (full program agenda right here). For these of you attending, we hope you learn our take under on the state of the buyer electronics trade and supply on-floor suggestions. Our thesis is that with practically $4 trillion in market capitalization, Apple is within the driver’s seat and everybody else is a passenger (and Apple has a minimal presence at CES). Extra under.

The final full Temporary (right here) generated numerous responses on two fronts: 1) from Cedar Rapids residents, previous and current, who share our fondness of the Quaker Oats Christmas tree, and a pair of) from many feedback on the way forward for the entry edge. A kind of feedback which we didn’t point out in that Temporary was that the entry edge is rising as a result of some parts of conventional knowledge facilities are shrinking and localized edge processing is the product of continued processing, storage, and different technological enhancements. We expect that time, plus feedback concerning the huge variations in electrical energy availability and costs, needs to be added to the earlier Temporary’s thesis.

Additionally, since it is a Vacation week and typically the workplace could be much less busy, listed below are two very latest discussions that we might counsel watching/ listening to as time permits.

- Chris Penrose, former 30+ 12 months AT&T govt and now International Head Enterprise Improvement – Telco for Nvidia, on the TelcoDR podcast referred to as Telco in 20 (right here). In addition to a really fascinating software of sovereign AI (synthetic intelligence) for Indonesia, he discusses the preliminary outcomes of the Softbank discipline trial (press launch right here).

- Bob Yates, who was SVP of M&A for Stage(3) Communications from 1999-2011, seems on Dan Caruso’s podcast referred to as The Bear Roars (right here) together with Dan’s upcoming guide referred to as Bandwidth: The Untold Story of Ambition, Deception, and Innovation That Formed the Web Age and the Dot-Com Increase (preorder right here on Amazon). There’s a second interview on The Bear Roads that’s equally entertaining from Stephanie Copeland of 4 Factors Capital, a long-time Denver telecom/ tech govt.

Lastly, we need to observe the passing of two necessary figures within the cable trade since our final Temporary. Dick Parsons, who was head of Time Warner after they merged with AOL and led the corporate (and plenty of others) by turbulent waters, handed away on December 26th (New York Instances obituary is right here). This morning, we realized by a Sunday Temporary reader that Chuck Dolan, a cable pioneer who began Cablevision and HBO, handed away at age 98 (Wall Road Journal obituary is right here). Each had been legends, and we are going to miss their wit and knowledge enormously.

The fortnight that was

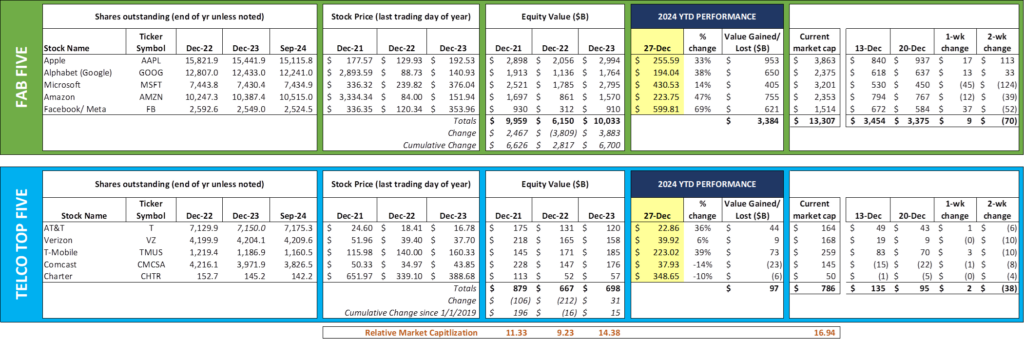

This has been a quiet week for each the Fab 5 (+$9 billion) and Telco Prime 5 (+$2 billion). Absent some vital rally or selloff, the Fab 5 will acquire $3.3-3.4 trillion in market capitalization in 2024, down from the $3.9 billion created in 2023. During the last six years, the Fab 5 have created ~$10 trillion in market worth. The Telco Prime 5, in contrast, created $100 billion in worth over the identical interval. Mentioned in a different way, for each greenback created by the Telco Prime 5 because the starting of 2019, the Fab 5 have created $100.

For the Fab 5, 2024 shall be generally known as the “Peak Yr of Combating the Authorities.” Nowhere is that this extra obvious than with Mountain View-based Google/ Alphabet, who’s presently going through the prospect of divesting their browser division (Chrome) in addition to many different restrictions (Bloomberg article outlining every of these modifications right here). Regardless of the looming modifications, the inventory gained $650 billion in worth, barely greater than 2023 ($628 billion).

Alphabet just isn’t the one one going through investigation. Microsoft was simply handed a really broad request for info from the FTC (article right here); Apple (The Verge’s wonderful protection right here), Amazon (partial dismissal of the FTC’s case in late September right here) and Meta (Reuters article right here on the 2026 trial date that would probably unwind their acquisition of Instagram right here) are all concerned in multi-year authorized actions.

Many have requested whether or not the investigation depth displayed over the past a number of years will proceed within the Trump administration. Whereas the precise reply won’t be recognized for a number of weeks, the Lawyer Normal nominee, Pam Bondi, doesn’t have the activist streak of the present lawyer basic or head of the FTC. Our guess is that activism shall be diminished, regardless of Jeff Bezos’ possession of The Washington Put up and the complicity of Meta in suppressing info on each Fb and Instagram that would have impacted the 2020 election in addition to COVID-related issues (every of which Meta CEO Mark Zuckerburg has admitted had been poor choices in a letter to the Home Judiciary Committee – see publish right here). Extra to come back, however we predict a pendulum shift again to the center-right.

Talking of regulatory actions, AT&T acquired some superb information final week from the Federal Communications Fee (FCC) as they permitted Ma Bell’s plan to switch conventional copper line native telephone service with AT&T Telephone Superior, a wi-fi native telephone different (Bloomberg article right here). Whereas this ruling applies to a handful of houses in Oklahoma, the precedent and blueprint established by an outgoing Democrat-chaired FCC units the stage for acceleration of copper retirement, a profit for each AT&T and Verizon’s telco items.

Lastly, there was a really intriguing article on Altice in Fierce Community which featured a quote by Nate Edwards (AT&T, Lumen, now Altice) that cable firms might compete in opposition to new broadband opponents utilizing cellular (we fully agree) and video. His premise is that the hole between streaming and linear broadcast methods is narrowing, and that bundling broadband, video and cellular could possibly be an efficient cudgel to firms reminiscent of Frontier (who could have FiOS linear TV providing after their merger with Verizon is permitted) and upstart FTTH suppliers.

Whereas the double-play (broadband + wi-fi) is sensible (see the final full Temporary right here on how we expect it’s going to affect AT&T), the incorporation of video as a essential bundle part is an actual headscratcher. Content material creators reminiscent of Amazon, Netflix, and Apple are writing huge checks. Comcast and Warner Bros. Discovery are additionally segregating their linear channels as part of a plan to (probably, in WBD’s case) spin or promote these items. Linear TV served because the content material aggregator for many years, however digital aggregators (together with Xumo, the brand new video platform for Altice) are taking on. We expect that Nate’s feedback would possibly assist Altice with sure segments, and positively will assist scale back the substantial churn Altice has skilled, however linear video is at greatest a distant third half to what shall be a broadband+wi-fi play.

CES preview—AI helps however doesn’t remake the buyer electronics trade

There shall be numerous dialogue on the upcoming Shopper Electronics Present about how synthetic intelligence will remake the trade. “Mix a superior mass market massive language mannequin (LLM) with respectable {hardware} specs and the trade construction will basically change” is the favored thought.

Whereas we agree that AI shall be a robust drive and drive handset upgrades because it turns into an indispensable a part of society, it doesn’t upend the present client electronics construction which is dominated by Apple. As we mentioned in our opening feedback, the Cupertino big, with practically $4 trillion in market capitalization, has probably the most to lose if AI proves to be revolutionary, they usually have the stability sheet and market share to make sure that any developments profit the iPhone enterprise mannequin.

Whereas now we have not mentioned this shortly, listed below are three issues we expect has made Apple profitable because the launch of the Macintosh in 1984:

- Being as tightly built-in (closed) as attainable. From the start of the corporate, software program integration into {hardware} has been tightly managed. Whereas many causes are cited (together with safety, effectivity, person expertise and value), the end result is similar: Apple views their product as a mixture of {hardware} and software program. We don’t suppose that basis will crumble due to a wave of AI apps.

- Creating merchandise that may be simply marketed. Apple turned computing into one thing that was “cool” within the Eighties and reinvented the music trade in 2000s with the launch of iTunes and the iPod. The phrase “A thousand songs in your pocket” nonetheless stands as one of the crucial highly effective product tag traces in client electronics historical past. The iPhone turned Apple into a world aspirational model and compelled Apple to work with tons of of wi-fi carriers working a myriad of networks throughout dozens of spectrum bands. They eliminated community compatibility as a barrier to buy – no small feat.

- They weren’t _________. Within the early days, that clean was stuffed by Microsoft (queue the Mac vs PC adverts). As their market management has grown, overtly direct comparisons to particular firms (and even the Android working system) have pale into the background. We see T-Cell’s “Challenger to Champion” mantra as an try and observe Apple’s transition.

There are various extra components to Apple’s success that we don’t have time to debate on this column, a few of that are straight attributable to Tim Cook dinner. However the three talked about above, mixed with the traits of profitable massive language fashions, lead us to imagine that Apple is greatest positioned from a product perspective to benefit from AI’s advantages. Right here’s why:

- Apple singularly has the potential to introduce localized AI fashions which might be materially extra responsive and customized than every other firm. We don’t have the precise statistic however could make an informed guess that no less than 1 / 4 of the acknowledged capability of an iPhone 16 goes unutilized in the course of the lifetime of a median iPhone person. What might Apple do with 30-60-90-120 GB of native reminiscence? Rather a lot. Contemplate that all the Oxford English dictionary consumes just below 600 MB of capability. And, due to their tight integration of iOS and the iPhone {hardware}, localized AI shall be environment friendly and responsive.

- Apple, by Siri, has already been skilled to reply to questions in 22 languages (and rising). The iPhone, per this latest Bloomberg interview with CEO Tim Cook dinner, launched the corporate to tons of of thousands and thousands of latest customers throughout the globe. Siri, now barely greater than a decade previous, has been bettering its syntax and dialect. It is probably not pretty much as good as another assistants, however it’s the most ubiquitous. With elevated AI utilization, Siri’s voice recognition will enhance sooner than others. We began to see a few of the enhancements to Siri within the newest iOS launch (Voice Management deep dive from Potential Internet right here). Warts and all, Apple would relatively have a skilled assistant than begin from scratch.

- Apple has a loyal and huge developer neighborhood. We expect that is probably the most essential component for the buyer market. Native processing (with assist for extra advanced queries from OpenAI and different LLMs), together with a world addressable market improves the financial alternative for builders. In consequence, Apple Intelligence turns into a number one LLM practically in a single day.

Apple’s problem just isn’t from AI itself, however from the embedded base of connecting units that don’t have related processing capabilities. TVs are getting cheaper however not smarter – the intelligence is coming from peripheral units like Xumo, Apple TV, Fireplace, Roku, and others (and every of those platforms has very completely different improvement roadmaps). What if the peripheral had been embedded in a brand new, smarter show? We are able to’t assist however suppose that Cupertino has been pondering loads about show consistency, and an entire rethinking of how we view content material is simply too huge of a possibility for Apple to disregard.

Latest stories would additionally counsel that Apple is critically contemplating a competitor to Amazon’s Ring and Google’s Nest franchises. Simply earlier than the Christmas Vacation, Mark Gurman of Bloomberg reported that Apple is contemplating a six-inch show that might combine facial recognition (presumably by one’s Apple ID) into good locks. This sounds small however would firmly tie iOS to the house. One might simply see an integration of Apple CarPlay to storage door opening or paying for occasion parking. Whereas it is probably not a big line of enterprise, a wise door additional cements the worth of Apple to its embedded base.

Backside line: CES continues to evolve as expertise advances. Apple lacks some essential parts of the in-home electronics expertise (e.g., PlayStation or Xbox equal; dwelling home equipment like LG and Samsung), however the firm influences the buyer electronics trade greater than every other. Not like different {hardware} firms which give attention to producing right now’s expertise cheaper, Apple creates differentiation by software program integration. This fusion creates a excessive barrier to entry and gives a really robust argument for continued market capitalization acceleration. Reasonably than making a extremely disruptive and disintermediating surroundings, AI really makes Apple’s management stronger.

That’s it for this week. We are going to dig into earnings drivers in our subsequent full Temporary (January 12). Till then, in case you have associates who want to be on the e-mail distribution, please have them ship an electronic mail to sundaybrief@gmail.com and we are going to embrace them on the listing (or they’ll join straight by the web site).

Lastly – go Davidson Faculty Basketball and Kansas Metropolis Chiefs!

Vital disclosure: The opinions expressed in The Sunday Temporary are these of Jim Patterson and Patterson Advisory Group, LLC, and don’t replicate these of CellSite Options, LLC, or Fort Level Capital.