Cement Produces Unavoidable Emissions

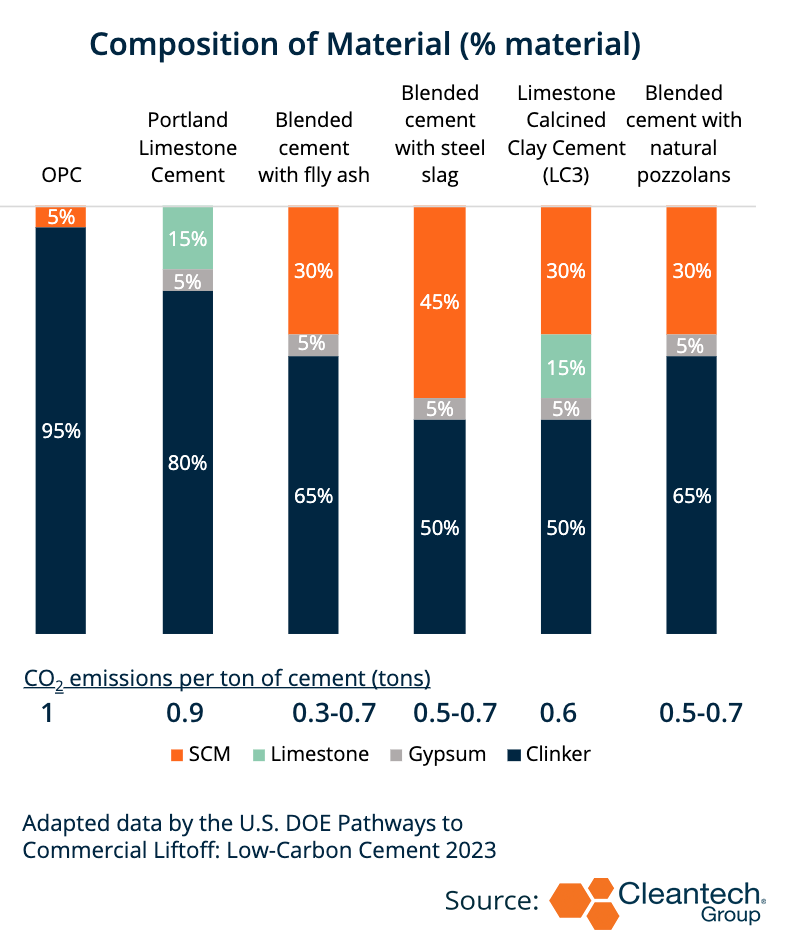

Second solely to water, concrete is essentially the most consumed materials on Earth with an annual manufacturing of roughly 4 billion tons. The business is liable for 7% — 8% of worldwide anthropogenic emissions and over 3% of the overall international power manufacturing. Ninety % of concrete’s emissions come from its main ingredient, cement, that produces 1 ton of CO2 per ton of cement.

Whereas main producer firms report plant-level information, monitoring 100% of emissions from the business is presently unfeasible. 60% of emissions are as a result of limestone calcination the place limestone (CaCO3) decomposes into CO2 and lime (CaO). An extra 40% of emissions come from the burning of fossil fuels to succeed in kiln temperatures of two,000° C or extra, and different small steps.

Options at varied phases of growth are rising however usually are not on monitor to fulfill net-zero by 2050. The business goals to cut back 20% of CO2 emissions per ton of cement and 25% of CO2 emissions per ton of concrete by 2030. In 2022, the discount of CO2 per ton of cement was solely 2.2%, nicely under the goal. To satisfy these objectives, cumulative investments of $20B by 2030 are required for low-carbon cement options and $60B — $120B by 2050, says the World Cement & Concrete Affiliation (GCCA).

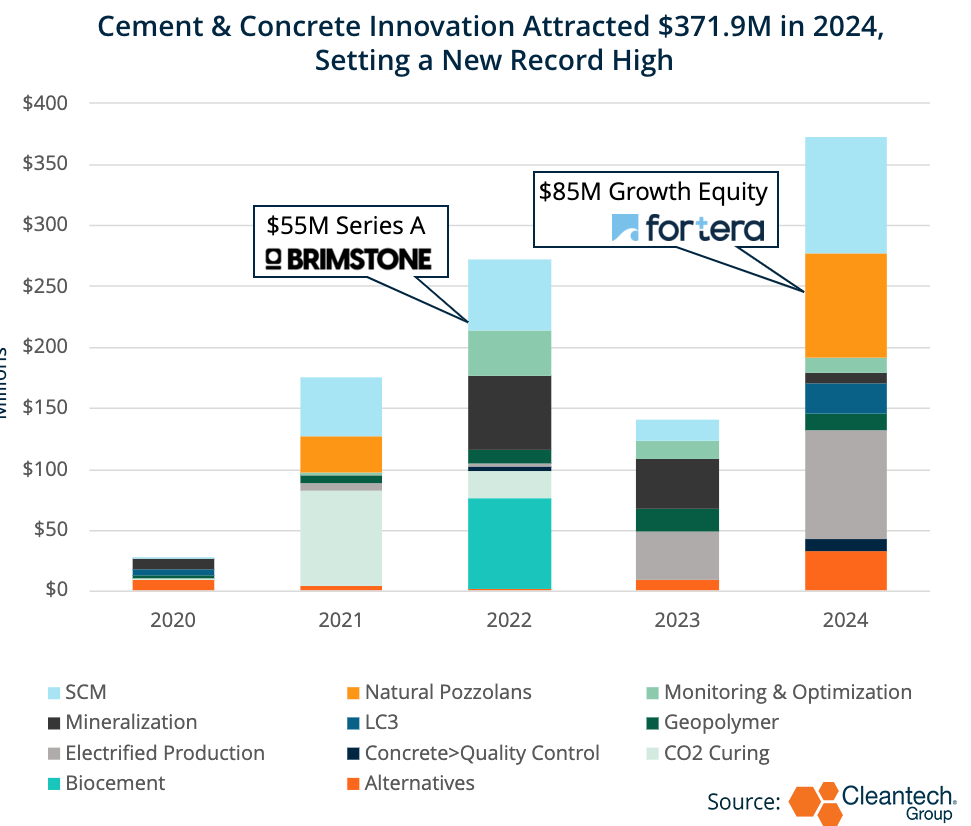

The excellent news is, we tracked a record-breaking yr in cement innovation in 2024. The highest options embrace however usually are not restricted to clinker substitutes, different gasoline sources, and carbon seize.

Clinker Substitutes

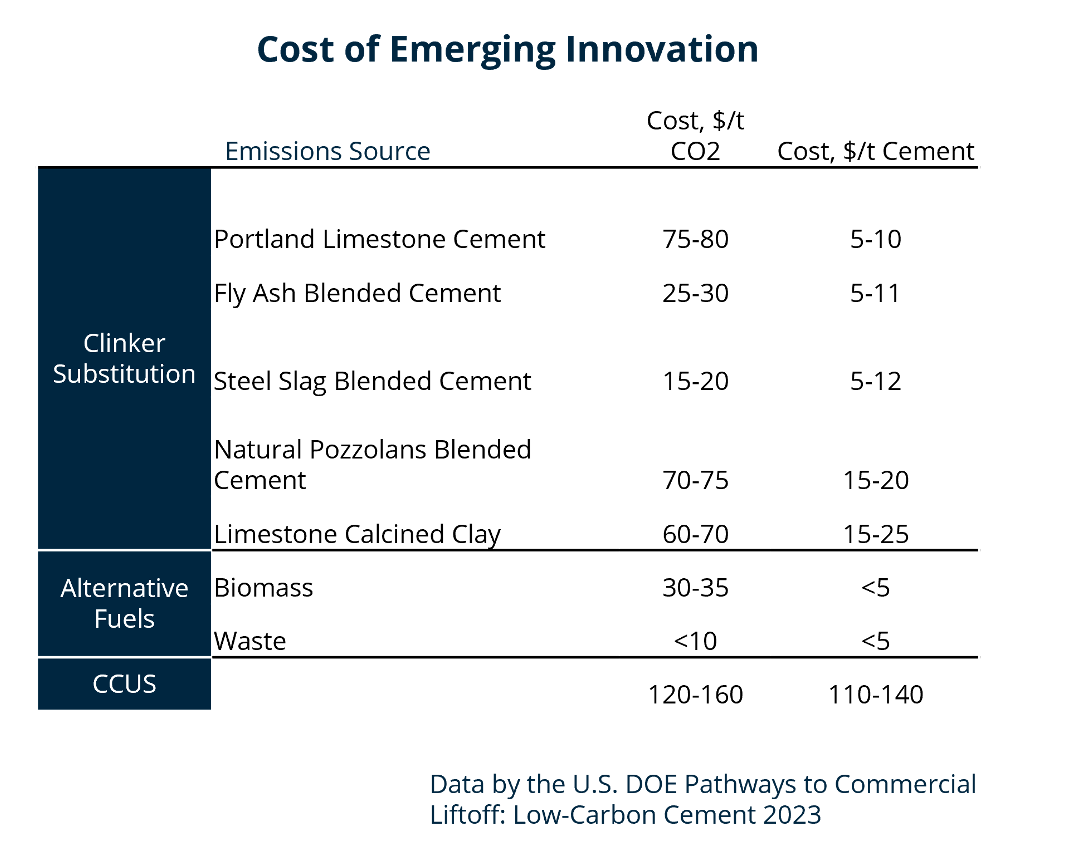

There are maturing and commercially deployed options that combine industrial supplies from mining, building, demolition, hazardous and even agricultural waste. These substitutes are generally known as Supplementary Cementitious Supplies (SCMs) and there are a whole lot of examples. Typical cement ranges from $30-$80/ton whereas low-carbon cement is $65-$130/ton. Low-carbon cement averages a 75% premium in comparison with typical cement. Use of different broadly obtainable and cost-effective sources like low-grade clays or pure pozzolans (volcanic rock) are popularizing.

Carbon Upcycling sequesters CO2 into reactive feeds together with crushed glass, fly ash, and metal slag for utilization in concretes and different high-value merchandise like plastics and coatings. It’s presently piloting its expertise at CRH’s Canada Mississauga cement plant after receiving investments from CRH Ventures in 2023. Carbon Upcycling can also be piloting its expertise with Holcim, CEMEX, TITAN Cement Group, and others.

Alt Fuels & Electrification

These fuels could also be derived from a mix or the whole use of business waste supplies, by-products, or biomass. They add $5-$10/ton cement on common and are at a TRL 9. Different low-carbon gasoline sources like inexperienced hydrogen produced through electrolysis are exceedingly costly with a TRL 5-6, however might in the future have an effect.

Electrification is close to a TRL 3, however whereas nonetheless early in growth, it may possibly considerably offset carbon emissions by as much as 40% — 87% or extra when utilized in mixture with pre-calcined uncooked supplies. Precise electrification prices are tough to calculate as a result of varied parameters which are particular to location and output however will be 27% — 45% of the overall price per ton of cement.

CemVision reuses industrial waste as a uncooked materials, sometimes from metal slag and mining waste, and makes use of electrical ovens or plasma. It’s recommissioning failing cement vegetation throughout Europe by retrofitting with electrification after which producing its low-carbon cement. CemVision is nearing a pilot demonstration in 2025 with a 4,000 ton per yr capability.

Carbon Seize

Level Supply Seize (PSC) for industrial emitters is a commercially deployed answer obtainable to the cement business proper now. Until you’ve acquired $1B to construct a seize facility, then PSC is essentially the most viable and solely choice. This expertise is scaling quickly with extra widescale adoption to come back within the early 2030s. Different seize applied sciences like Direct Air Seize (DAC) are considerably dearer and won’t ramp up till the 2040s. The most important and first seize facility particularly concentrating on cement emissions started operations in January 2024 at CNBM’s facility in Qingzhou Zhonglian, China with a 200,000 ton per yr capability.

Carbon seize will be built-in, as within the case of Leilac. Its expertise heats limestone through a particular reactor the place furnace exhaust gases are saved separate from course of gases. This allows the seize of pure CO2 as it’s launched from limestone. There’s additionally potential for electrification of calciner to cut back the emissions from gasoline. Leilac is deploying a first-of-a-kind facility along with its mum or dad firm, Calix, in South Australia to provide near-zero emissions lime and provide captured industrial CO2 emissions to the Photo voltaic Methanol Venture for the creation of low-carbon transport fuels for the transport sector.

Carbon seize can also be carried out post-combustion to seize the emissions from flue gasoline. Ardent’s gasoline separation expertise utilizing membranes can exactly filter CO2 from flue gasoline. Its expertise is compact and modular, becoming inside any cement facility. It has even mentioned deploying its expertise in a Seize-As-A-Service (CaaS) mannequin whereby emitters don’t need to entrance excessive capital expenditure. Quite, Ardent will act as a seize service supplier. It’s raised over $16.5M from Solvay Ventures, Chevron Expertise Ventures, Technip Ventures, and extra.

Excessive CAPEX and Few Financial Incentives Have Slowed Progress

Cement is a $410B business, and the demand for it’s set to extend, particularly in growing areas in Africa and Asia. Assembly these rising urbanization calls for would require much more scale up of the present capability. Extraordinary Portland Cement (OPC), the standard cement composition, is taken into account the one materials to fulfill these calls for. That is because of the vast availability of an essential and low cost ingredient, limestone.

It’s no coincidence that metropolitan cities are all the time inside an earshot of a limestone mine or quarry. This co-location helps carry down the price of transport and storage to the areas with highest demand. However this has resulted in regionally fragmented markets (usually a 200 km radius) dominated by only some incumbents who’ve near-complete management over their respective provide chains. Solely 3% of the worldwide cement manufacturing was low carbon cement materials in 2023, which means that 97% of the market is ready to be focused, in keeping with the Worldwide Power Company.

For innovators deploying clinker substitutes, they should be co-located close to a quarry through partnership with a requirement proprietor. With out it, scale up of business volumes over 300 thousand tons per yr won’t ever be economically viable. This implies there’ll ultimately be vital consolidation to account for the geographic restrictions, just like the mineral mining business. Presently, there aren’t any projections of low carbon cement supplies ever with the ability to meet the calls for of urbanization in these areas.

In areas with entry to low cost and dependable sources of renewable power, we are going to see electrification, electrical energy, or plasma, will take off within the 2040s, in keeping with the Power Transitions Fee. However in different growing areas, electrification will likely be considerably too pricey for widescale adoption. In these areas, different fuels from agricultural waste and different sources will emerge as viable options to fossils. Incumbents like CEMEX and CEMENTA have already begun integrating biofuels. Equally, inexperienced hydrogen is a possible gasoline supply. However high-ticket prices for electrolyzers imply uptake within the near-term is unlikely.

Cement is an Infrastructure Drawback

After studying Deb Chachra’s “How Infrastructure Works,” I started to grasp extra of the complexities going through the important methods inside the cement and concrete industries. Constructing out any infrastructure is a monumental process, particularly with restricted financing choices for brand spanking new amenities or lack of assist from the general public sector, simply a few limitations that low-carbon cement options are going through. However why change the basics of cement manufacturing when all we actually want is to decarbonize the fabric and its manufacturing strategies—simpler mentioned than accomplished!