|

Take heed to this text  |

Whereas Work together Evaluation has much less favorable mid-term predictions for the AMR market, it’s nonetheless optimistic in regards to the long-term development. | Supply: Adobe Inventory

Work together Evaluation decreased its forecast for the worldwide cell robotic market by 18% in 2027 as a consequence of a sequence of macroeconomic elements it mentioned are impacting demand. This difficult local weather has resulted in producers and retailers slowing their funding into automation, and the analysis agency now not expects a speedy uptick in AMR deployments earlier than 2027.

In its newest report, Work together Evaluation outlines:

- How governments have struggled within the aftermath of the pandemic

- How the retail trade remains to be going by means of a post-Covid correction

- Why China’s economic system is weaker than anticipated

- How automotive has been hit by sluggish uptake of electrical autos

Work together Evaluation mentioned that these exterior elements, coupled with 60 nations holding elections in 2024 and battle in Ukraine and the Center East, have constrained demand for cell robots. Value declines are additionally slower than forecast, which has in flip slowed uptake, in keeping with Work together Evaluation.

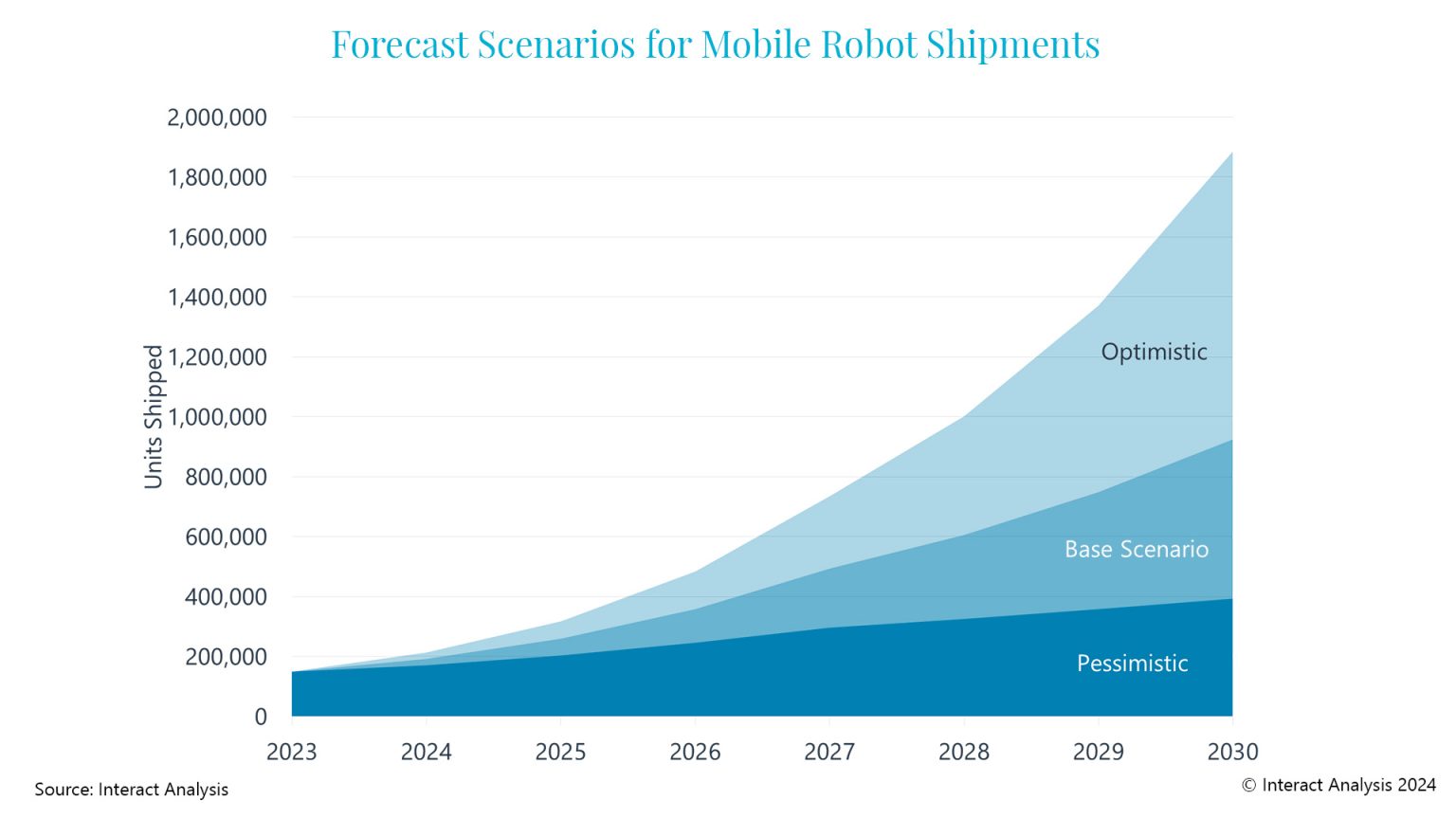

Regardless of its extra cautious forecast, the outlook for 2030 remains to be for double-digit development, and Work together Evaluation has created optimistic, base, and pessimistic situations.

In Work together Evaluation’ most bullish prediction state of affairs, cell robotic shipments may attain practically two million by 2030. | Supply: Work together Evaluation

What’s holding again cell robots?

Work together Evaluation’ survey of 300 consumers of cell robots reveals it expects automation spending to extend in 2024 by a imply common of 18% in contrast with 2023. It now forecasts buyer uptake will proceed to develop at a linear fee reasonably than exponential fee, whereas worth declines will likely be slower than beforehand anticipated as labor prices improve, stopping an avalanche in demand.

The trade has extended its post-Covid correction as customers return considerably to pre-2020 shopping for habits. Work together Evaluation additionally mentioned shopper spending has been impacted by excessive inflation and rates of interest. Nonetheless, firms are persevering with their automation plans to mitigate dangers related to labor shortages, rising wages, and financial uncertainties, guaranteeing enterprise continuity and resilience.

Cell robotic investments are by and huge getting a lot larger in dimension, and the related due diligence and inside scrutiny are prolonging gross sales cycles. Work together Evaluation mentioned this double-edged sword causes some turbulence for robotic distributors and, on the identical time, loads of upside potential.

With that in thoughts, Work together Evaluation predicts cell robotic revenues will attain $5.5 billion in 2024 and develop at greater than 20% yearly as much as 2030.

China sees sluggish development domestically

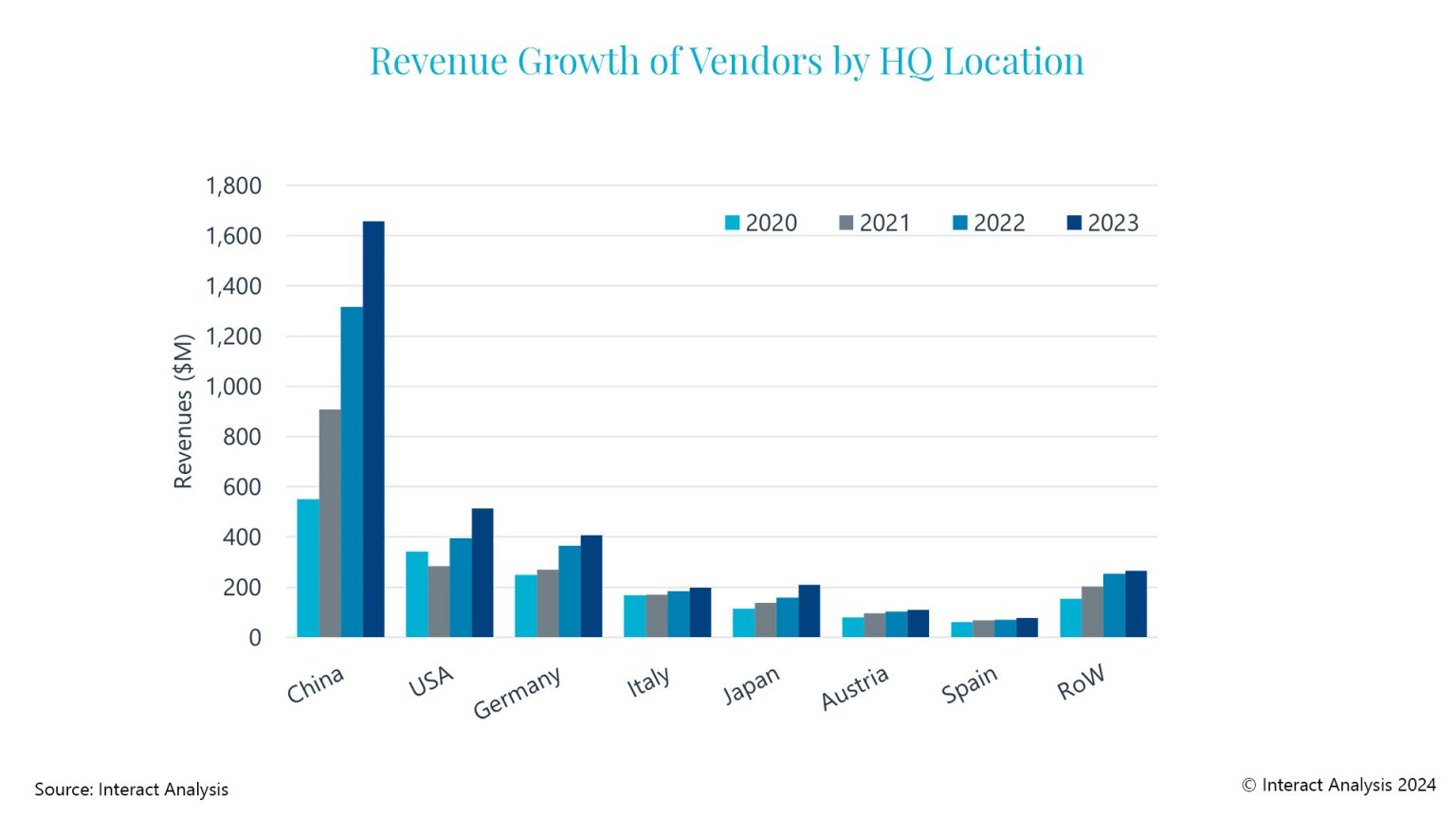

Work together Evaluation’ information on the income development of distributors by location reveals that Chinese language distributors proceed to dominate the worldwide cell robotic market. | Supply: Work together Evaluation

China remained the most important marketplace for cell robots in 2023, contributing over 70% to the rise in unit shipments – underscoring its position as a producing powerhouse. Nevertheless, as a consequence of decrease relative costs within the area, this accounted for less than 32% of the overall income improve, in keeping with Work together Evaluation.

Weakening home demand in China has accelerated efforts by Chinese language distributors to develop in worldwide markets, the analysis discovered. Growing discontent in Europe and the U.S. over Chinese language distributors undercutting home suppliers (outdoors of the cell automation sector) raises the prospect of tariffs being launched, which may additionally influence cell robots. Nevertheless, Work together Evaluation expects lately introduced stimulus insurance policies in China to spice up home demand over the following few years.

Chinese language distributors proceed to dominate the worldwide cell robotic market, producing practically 50% of all international cell robotic revenues and two-thirds of shipments in 2023. Firms like Geek+, HikRobot, and Quicktron lead the market, with sturdy development each domestically and internationally.

Regardless of quite a few acquisitions, Work together Evaluation mentioned the cell robotic market isn’t consolidating, as most acquisitions up to now are by non-mobile robotic firms. For instance, Rockwell Automation acquired Clearpath Robotics and OTTO Motors. Extra distributors emerge annually and extra industrial firms are launching AMRs, so the share of the highest 10 and high 20 main distributors has barely modified since 2018.

Labor shortages, rising prices drive cell robotic demand

Work together Evaluation initiatives the put in base of cell robots to exceed 4.2 million on the finish of 2030, with practically 1 million to be added in 2030 alone (and this excludes these utilized by Amazon). The labor scarcity stays the largest driver of demand for cell robots, exacerbated by rising labor prices and the near-shoring and re-shoring of producing.

Nevertheless, excessive upfront prices, lack of interoperability, competitors from mounted automation, and rising inflation and rates of interest are vital boundaries to cell robotic adoption. Lowering costs and the introduction of Robotics-as-a-Service (RaaS) and leasing fashions are serving to to beat these hurdles.

Regardless of the much less favorable mid-term outlook, Work together Evaluation nonetheless anticipates double-digit income development of 20-30% yearly out to 2030 and the general long-term image stays optimistic. This follows the expansion of shipments in 2023 of 23%, reaching nearly 150,000 over the yr.